Fundraising event compliance is an often-overlooked yet essential aspect of raising money for your school. Learn the essential compliance requirements here.

Discover AI Summary

• Keep your donors happy and protected by clearly stating the Fair Market Value (FMV) of any gifts or services they receive at events; this ensures their tax deductions are accurate and builds lasting trust for future campaigns.

• Before launching your next fundraising event or online appeal, always confirm if your institution needs to register for charitable solicitations in every state where you're asking for donations, as failing to do so can lead to big fines and reputational damage.

• Be aware of Unrelated Business Income Tax (UBIT) for activities that regularly generate revenue not directly tied to your educational mission; if you hit certain thresholds, you'll need to file extra paperwork to stay compliant.

• Don't let local regulations derail your event success; make sure you secure all necessary state and local permits for activities like raffles, auctions, or games of chance to avoid an embarrassing shutdown and protect your alumni engagement efforts.

• Proper record-keeping and timely, detailed donor acknowledgments for contributions over $250 are non-negotiable; this not only helps donors with their taxes but also reinforces their loyalty and trust in your institution.

• If navigating these complex compliance rules feels overwhelming, consider bringing in a compliance expert, which can free up your advancement team to focus purely on building relationships and driving your fundraising mission forward.

From annual galas to class reunions, there are numerous benefits to hosting events for alumni, parents, and other members of your school’s community. These fundraisers are mission-critical, generating the vital resources necessary to move your institution forward.

However, high engagement and an influx of fundraising dollars can easily overshadow a non-negotiable element of event planning: compliance.

Fundraising event compliance is a fundamental infrastructure that protects your school and strengthens donor trust. Not to mention, the consequences of failing to properly manage the legal and tax requirements of a fundraising event can be severe.

This guide details the core compliance pillars that your fundraising officers must prioritize for successful events.

Charitable solicitations registration is the foundational state-level requirement for nearly every nonprofit organization that solicits funds from the public. Registration is required in approximately 40 states, and organizations must register in every state where they conduct fundraising activities.

The registration process varies from state to state. For example, in Pennsylvania, educational organizations are exempt from registration if they meet specific criteria. Alaska, however, does not offer exemptions for educational institutions.

If your school’s state (or any state in which you’re fundraising) requires registration, the regulation likely applies to any solicitation activity targeting the state’s residents. According to Foundation Group, virtually all forms of revenue generation trigger a registration requirement. This can include:

While the rules for educational exemptions are inconsistent and often conditional, assuming an automatic exemption is a high-risk liability. Failure to secure and maintain registration—or proof of exemption—means the institution is soliciting illegally in that state.

The ramifications of non-compliance are serious. A state regulator can issue cease-and-desist orders, levy substantial fines and late fees, and, in extreme cases, demand the return of all funds raised illegally within their jurisdiction. For development officers charged with protecting alumni relationships and institutional reputation, the potential legal exposure and public scrutiny are not worth the administrative shortcut.

Tax-exempt status does not equate to tax immunity. Fundraising events are often subject to Unrelated Business Income Tax (UBIT) if they regularly generate revenue from activities that are not substantially related to the institution’s educational purpose.

Any tax-exempt organization that generates gross unrelated business income (UBI) of $1,000 or more during its fiscal year must file IRS Form 990-T. This form reports UBI to the IRS and indicates any tax due.

Educational institutions can determine whether a fundraising activity is subject to UBIT by considering:

Keep in mind that Form 990-T doesn’t take the place of an organization’s annual Form 990 filing—it supplements it. Failing to file both can result in severe penalties, such as having your 501(c)(3) status revoked.

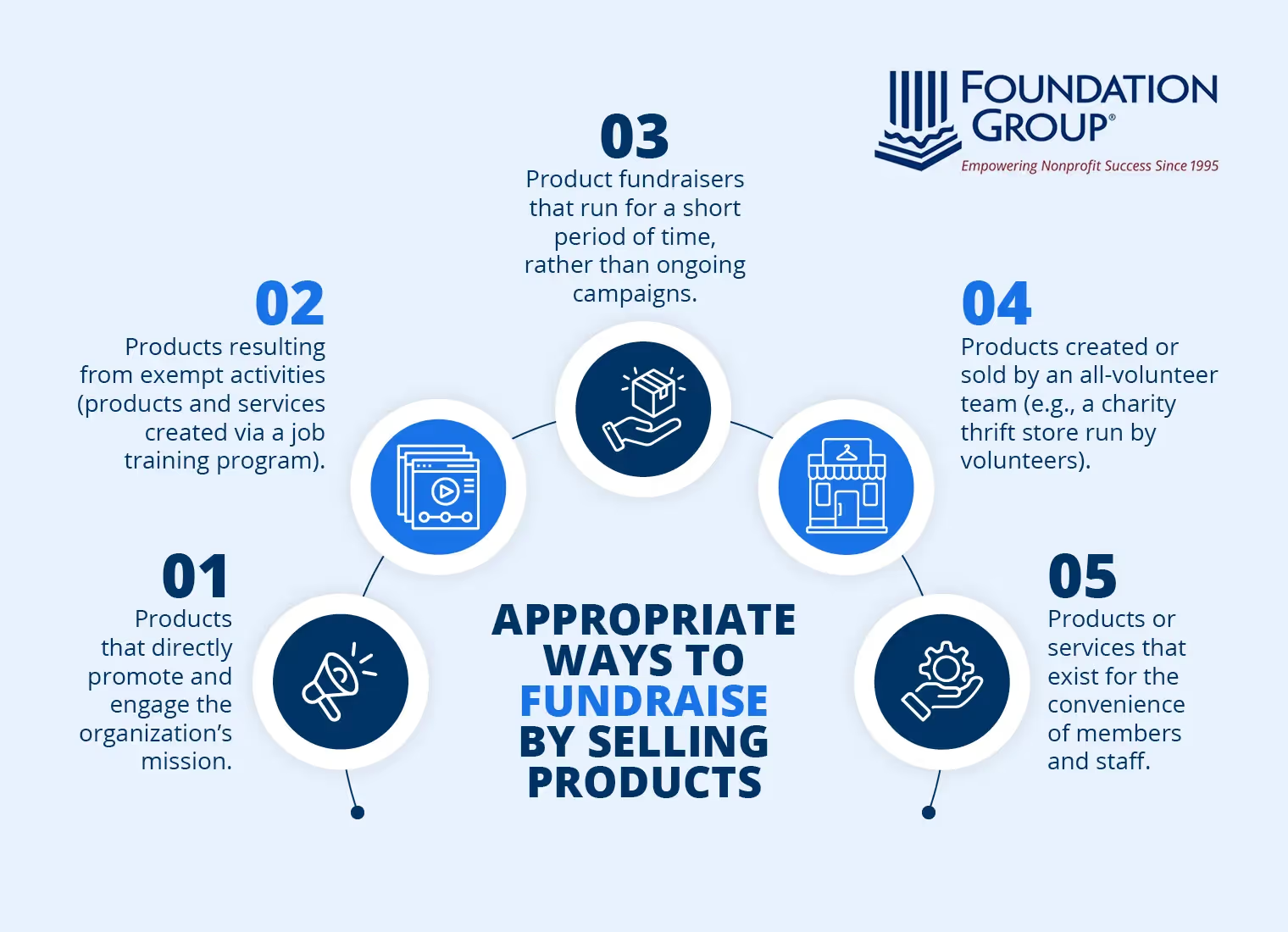

It’s important to note that not all product sales are considered UBI. See the image below for examples of products your school can sell:

The best way to ensure your school adheres to tax regulations surrounding product sales is to prioritize detailed recordkeeping. Sales data, such as total revenue generated and fundraising expenses, is crucial in determining whether the income qualifies as UBI.

The final layer of event compliance involves managing local-level rules that directly affect the donor experience and the legality of the event itself. This includes securing the necessary permits for games and auctions, as well as properly calculating how much a donor can deduct from their taxes.

Beyond federal tax and state charitable solicitation laws, fundraising activities involving games of chance are regulated heavily at the state and local levels. Raffles, lotteries, poker tournaments, and even certain types of silent auctions may be considered illegal gambling unless the nonprofit has secured specific state licenses or local permits.

Many jurisdictions require educational organizations to obtain a separate permit for each game of chance, often with a strict cap on the prize value or the frequency of the game. Local authorities can shut down an event in progress for lack of proper permits, creating a highly damaging public relations crisis for the institution and exposing event organizers to personal liability.

Every fundraising event that provides something of tangible value to the donor—a gift card, a round of golf, a seat at a performance—is considered a quid pro quo transaction. Fundraisers are obligated to inform donors exactly what portion of their payment is a deductible contribution and what portion represents the Fair Market Value (FMV) of the goods or services received.

For example, if an auction ticket costs $100, but the event includes a dinner that typically sells for $25, then only the $75 excess contribution is tax-deductible. Careful bookkeeping for nonprofits is critical for accurately calculating FMV and reporting it to donors.

The IRS requires organizations to provide a written acknowledgment for any contribution of $250 or more that includes the following information:

Incorrectly stating the FMV or neglecting to provide proper receipts places the burden of proof on the donor in an IRS audit. This can directly damage the relationship and trust your fundraising team has worked so hard to build, ultimately sacrificing your chances of retaining donors for future fundraisers.

Effective fundraising is built on a foundation of operational excellence, and compliance is the most essential element of that operation. With the right strategy and expertise, your school can achieve successful fundraising and capacity building.

Many organizations benefit from the expertise of compliance experts who specialize in the nonprofit regulatory environment. These professionals handle the painstaking administrative and legal requirements of compliance, allowing development officers to focus entirely on their mission.

Table of Contents

Subscribe

See how modern advancement teams bring alumni engagement and fundraising together.

We’ve talked in length about some good events and the event management or fundraising tools that can make them succeed consistently. This time, we’re taking a step back and at the basics of fundraising event planning.

In this blog, we’re going through the essentials to turn your fundraising ideas into successful events that don’t just reach your targets but create powerful memories to strengthen your cause. Let’s get started.

As with every advancement initiative, the goals are where everything starts and leads back to. We’ve talked about the importance of Smart, Measurable, Attainable, Relevant, and Time-based (SMART) goals in a past blog. While creating the goals that will define your fundraising event, keep the following questions your attendees would have in mind:

Apart from these questions, your available staff time, target audience, budget, and other upcoming institution events will play a big part in shaping your scope for your event. Take your time with this step as the right goals are the foundation of a successful event.

Depending on your audience, budget, and goals, you may choose from a variety of fundraiser ideas, such as:

No two events are truly alike, and depending on the success of your fundraiser, a bold new approach might just be your next hallmark annual event.

As you’re not just planning any event, how you want to introduce fundraising to your event is going to be very important. Remember, a fundraising event can have multiple revenue streams. For example:

Nowadays, institutions usually look to include diverse fundraising methods in their fundraisers. This is also where pairing the right event with the right fundraising method can greatly impact your raised amount.

Now that you know what type of event you want as well as how you’re going to raise funds during it, it’s time to put the right tools to work. Pretty much every modern institution uses a fundraising platform to streamline their events and fundraisers. These tools help you:

and much more.

Platforms like Almabase help streamline these logistical elements, allowing you more time and energy to focus on fostering genuine connections with your donors.

Now that the building blocks are coming into place, it’s time to decide on arguably the most important part of an event, the people. You’ll want to form a committee of people to take on and help with specific parts of the event including but not limited to:

Apart from the above, you’ll want to think about corporations, non-profits, and associations that may want to play a pivotal role in helping you bring your event to life.

Now that all the bits and bobs are there, it’s time to lock in a specific place and time. It seems fairly basic but keep in mind that:

You’ve got all the info ready to go. But it doesn’t mean anything if it doesn’t reach the right audience. And even if it does, what type of messaging should they receive and when should they receive it so that they truly feel like attending or giving? That’s where your event marketing comes into play. You’ll want to make use of channels such as:

and much much more to get your event and your cause heard. Make sure that your marketing emphasizes how your fundraiser can help your cause of choice.

Even the most tight-knit plans have a chance of going wrong. A 10-minute delay caused by faulty audio equipment might just be that small little factor that disinterests a potential first time donor.

These are good things to keep in mind but ultimately, your contingencies may have to be just as unique as your event.

Nowadays, the event doesn’t truly end when the last guest leaves. Following up with attendees is crucial to maintaining their engagement and potentially turning them into loyal supporters. Post-event action items include:

Gratitude and proactive follow-ups go a long way in building long-term relationships with your supporters.

The ultimate measure of a successful fundraising event isn’t just the dollar amount raised but also the connections made and how deep those connections go over time. To turn your attendees into loyal supporters, you’ll want to consider some steps such as:

By nurturing these relationships, you're creating a network of passionate supporters who are more likely to advocate for your cause and contribute to future initiatives.

Fundraising events have certainly not gotten any easier to plan and host in the past few years. Donors and alumni in general simply expect more, and you can’t just rely on your long-time donors alone. However, we hope that this guide, despite just scratching the surface, was able to give you some ideas for your next fundraising event.

If you’re looking for a partner to help you manage events, engage alumni, and raise funds, do give us a shout and we’ll happily walk you through how we can help with your own personalized demo! ⤵️

How to Plan a Fundraising Event to Maximize Donations

Learn how to craft successful fundraising events step by step. Maximize donations with actionable strategies and engage donors meaningfully.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Your fundraising team just spent 40 hours planning a successful gala that raised $250,000. Now they'll spend another 40 hours manually entering guest lists into spreadsheets, reconciling payments across multiple systems, and sending individual thank-you emails.

This is the hidden cost of manual event workflows. While manual processes might seem like a cost-saving measure, they drain staff time, increase error rates, create HIPAA compliance risks, and pull your team away from what matters most: building donor relationships.

Hospital fundraising teams lose nearly five hours every day to these repetitive tasks. Almabase's fundraising event management software eliminates manual data entry, keeps Raiser's Edge NXT data in sync, and can save hundreds of staff hours each year.

Hospital fundraising teams rely on galas and events to fund critical programs, but manual processes drain staff time, increase the risk of errors, and make it harder to measure results accurately.

Here are just five ways your hospital foundation loses opportunities, revenue, and time by relying on outdated manual processes to manage your galas, golf tournaments and other fundraising events.

Manual workflows force staff to re-enter information across multiple systems — CRMs, payment systems, spreadsheets, and more. One analysis found that nonprofit staff spend up to 50 percent of their time on manual data entry. This kind of work is boring, wasteful and can lead to burnout.

Almabase’s TrueSync™ integration with Blackbaud Raiser’s Edge NXT and Blackbaud CRM reduces manual handling of sensitive records while maintaining clean, consistent data across systems.

A gala can generate thousands of data points, from attendee names and guest additions to dietary preferences and sponsorship tiers. That leaves too much room for error, since there are errors in about one percent of manual data entry keystrokes.

The result is delayed or missed donations and inconsistent communications—a major turnoff for donors. These mistakes often ripple downstream, leading to inaccurate reports and missed follow-ups that weaken donor trust.

Every hour spent on repetitive administrative work, like re-entering event registrations or sending one-off acknowledgments, detracts from opportunities to build meaningful donor relationships, plan strategic campaigns, and focus on high-impact activities that drive ROI for your organization.

Nearly 75% of nonprofits report persistent job vacancies tied to heavy workloads and manual processes. But one study found that turnover drops significantly when organizations shift away from the soul-sucking “busy work” of manual processes.

Many third-party vendors aren’t HIPAA-compliant or won’t sign BAAs—making them risky for fundraising for healthcare. Almabase’s HIPAA-compliant event registration platform is designed specifically for healthcare foundations, maintaining data security and compliance while integrating seamlessly with Raiser’s Edge NXT.

Trying to manage event registration, ticketing, and communications manually creates major inefficiencies.

Almabase’s event management software gives hospital foundations a single, HIPAA-compliant event registration software solution to handle every step from setup to stewardship.

For teams used to navigating disconnected tools, the results are immediate: faster event setup, fewer errors, and greater visibility into event ROI. Dashboards track participation, sponsorships, and giving in real time, helping staff quickly identify top prospects and follow up while engagement is fresh.

Key Benefits:

Almabase’s ticketing software for healthcare simplifies operations and keeps all event data connected to Raiser’s Edge, allowing fundraisers to spend more time on what matters—strengthening relationships and driving impact in healthcare fundraising.

Hospital foundations juggling multiple systems from spreadsheets to payment platforms and CRMs often leave staff buried in administrative work instead of engaging donors. Almabase eliminates that burden by creating a single, accurate source of truth so teams no longer need to chase down lists or reconcile records after every gala.

By automating event ticketing and maintaining HIPAA secure event registration, Almabase helps foundations run compliant, efficient, and mission-focused events that fuel sustainable fundraising for hospitals.

See how Almabase's fundraising event management software helps hospital foundations save hours, ensure compliance, and raise more funds.

Almabase replaces time-consuming manual workflows with automation that integrates every step of your event management process. Hospital foundations can set up event registration, ticketing, sponsorships, and communications in minutes—not weeks—through one platform that syncs directly with Raiser’s Edge NXT.

That means no more redundant data entry, disconnected spreadsheets, or manual imports. Event data, donor engagement, and payments all flow seamlessly in real time, ensuring accuracy and saving hours of administrative work.

Yes. Almabase is built with healthcare fundraising compliance in mind, offering SOC 2 Type II certification and Business Associate Agreement (BAA) support to meet HIPAA standards. The platform separates patient health information from donor engagement data, so hospital foundations can manage events, donor communications, and grateful patient programs securely and confidently. Compliance, data protection, and privacy are embedded into every workflow.

Through TrueSync, Almabase’s bi-directional Raiser’s Edge NXT integration ensures that all guest registrations, donations, and communications automatically sync with your CRM. This eliminates data duplication, reduces reporting errors, and gives fundraising teams real-time insights into donor engagement and event ROI. It also allows fundraisers to identify follow-up opportunities faster—translating event participation into sustained donor relationships.

Five Hidden Costs of Manual Event Workflows in Healthcare Fundraising

Stop losing hours to manual event work! Discover the Five Hidden Costs of manual gala operations, including HIPAA compliance risks and staff burnout. See how Almabase saves time for hospital fundraising teams.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

November 6, 2025

12 minutes

2024 was an interesting year for fundraising professionals. Persistent and emerging challenges in the nonprofit landscape coincided with some. While some issues carried over from previous years, new dynamics reshaped the way organizations navigated their work.

Last year was a year of highs and lows for fundraising and advancement professionals. From staffing struggles to shifts in donor behaviors, the year brought challenges that tested the resilience of nonprofits across sectors. However, these hurdles also paved the way for innovation, collaboration, and strategic rethinking, setting the stage for what 2025 might bring.

The donor landscape in 2024 presented an interesting problem. While overall donations increased, the donor pool continued to shrink. According to the Association of Fundraising Professionals (AFP), there was a 2% increase in total donations but a 4.5% decline in the number of individual donors. This trend posed a significant challenge for nonprofits reliant on a broad donor base for smaller, recurring contributions.

Staffing shortages and high turnover rates continued to be among the most pressing concerns for nonprofits in 2024. According to a study by NonProfit PRO, nearly 70% of nonprofits reported struggling with staffing challenges, citing underfunding and burnout as primary drivers.

This crisis was compounded by the competitive job market, which made it difficult for nonprofits to attract and retain talent. High turnover negatively impacted team morale and operational efficiency, forcing many organizations to stretch already limited resources to achieve their goals.

The rise of AI and other tech tools has been both a blessing and a challenge for nonprofits. While AI offers powerful capabilities—from predicting donor behavior to automating administrative tasks—it also requires significant investment in training and implementation. Many teams struggled to fully integrate these tools due to lacking technical expertise or financial resources.

The use of AI also brings forward some ethical concerns that increasingly became relevant throughout the year. There exists the risk of over-automating donor communication, which could lead to a loss of the personal touch that is central to alumni engagement. For smaller organizations, the hype around AI could also lead to investments in tools that did not align with their needs, diverting funds from more pressing priorities.

Despite the challenges, nonprofits showcased remarkable resilience. Many embraced hybrid fundraising models, combining virtual and in-person events to engage a broader audience. Charity Digital reported that organizations leveraging digital tools for storytelling and donor engagement saw significant returns on investment.

Additionally, DonorBox emphasized how nonprofits that invested in robust donor communication tools experienced improved retention rates, especially during year-end campaigns.

As we move into 2025, nonprofits more than ever need to build on the lessons of 2024 by focusing on sustainable growth and strategic innovation.

Resilience emerged as a defining characteristic in 2024, and nonprofits should ideally look to build upon it by adopting sustainable strategies and scalable practices, to better navigate uncertainty and a world that’s throwing a lot of innovations at us without leaving us much time or resources to consider our approach to each of them. With all that being said, we’d like to explore some broad focus areas that teams and institutions alike should watch out for in 2025:

The excitement surrounding AI and other technologies in 2024 often led to unrealistic expectations for nonprofits. A research paper published by Lauri Goldkind, Joy Ming, and Alex Fink critically assessed AI’s role in human services, questioning whether it offered genuine value or was simply a trend driven by hype. The study concluded that while AI holds transformative potential, it requires proper alignment with an organization's size, mission, and resource constraints to be effective.

Throughout 2025, Nonprofits should be shifting focus toward scalable and budget-conscious technology solutions. For example, a hypothetical smaller team that only needs a CRM and basic analytics could leverage low-cost digital tools and achieve better outcomes if these tools are customized to their specific workflows and objectives, as opposed to trying to cover all their bases and wasting both resources and time spent on upskilling.

The staffing crisis doesn’t seem to be letting up anytime soon with 68% of organizations reporting difficulties with recruitment and retention in 2024. Common challenges include toxic work cultures, burnout, uncompetitive salaries, and insufficient training opportunities. Increased investment in professional development, equitable pay structures, and supportive workplace cultures have been big talking points for a while but now they need to become key priorities. Policies aimed at reducing burnout, such as flexible work schedules and mental health support should be a good starting point.

Additionally, peer mentoring and community-building efforts are gaining traction. Nonprofits can leverage mentorship programs and peer support networks to foster a sense of community within their teams, leading to improved job satisfaction and retention.

At the heart of every nonprofit is its people—the staff, donors, and volunteers whose collective efforts drive change. By fostering positive internal cultures and focusing on impactful strategies, nonprofits can inspire trust and loyalty, ensuring their mission thrives in the years to come.

Nonprofits have responded to the recent donor market shifts by focusing on deepening relationships with existing donors. Strategies such as targeted communication and personalized outreach have since become standard practice. 2025 should be a good year for teams to consolidate knowledge of their tools and long-term goals so that they continue fostering donor loyalty seamlessly. A key area of focus will be on small and medium-sized donors and how teams can turn them into loyal donors moving forward.

With federal budget cuts for nonprofits and institutions seeming likely on the horizon, advancement and nonprofit teams especially in the US will need to explore sustainable alternatives to reach their goals.

That’ll just about do it for now but with 2025 seeming a difficult year to predict, there should certainly be a lot more to talk about in the coming months.

Key focus areas for fundraising in 2025

2024 was an interesting year for fundraising professionals. We go over some of the key learnings from last year to figure out key focus areas for 2025.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

.svg)

.webp)

.webp)

%20(1).webp)